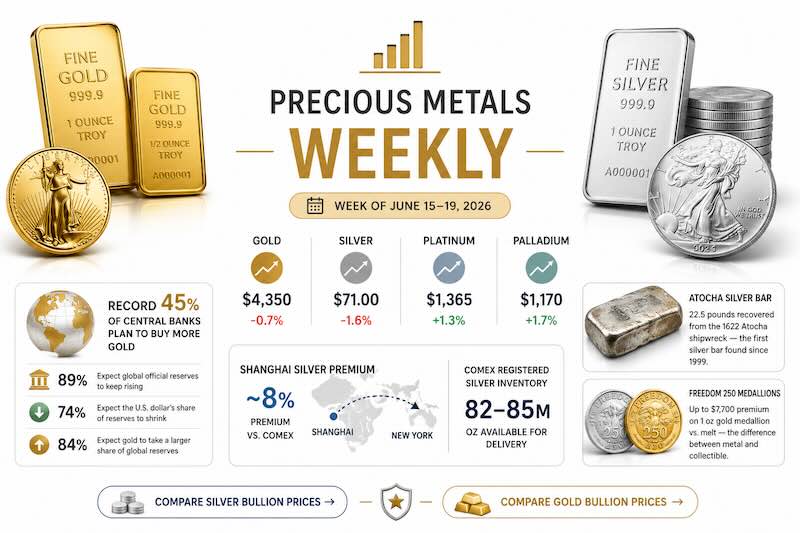

Week of June 15–19, 2026 (prices as of Friday; June 19 is Juneteenth, so U.S. markets are closed and quotes are thin)

Gold and Silver This Week

Two opposing forces ran through the metals this week. The first arrived Monday, when Washington and Tehran announced an interim peace agreement: a memorandum of understanding that opens a 60-day negotiating window and sets up the reopening of the Strait of Hormuz, the chokepoint for roughly a fifth of seaborne oil. Brent crude fell about 5%. That pushed gold and silver higher rather than lower, and the logic ran through the Fed — cheaper oil means less inflation pressure, and less reason to hike. The implied odds of a December rate hike dropped from near 90% to about 60% in a single session. Gold climbed roughly 3% above $4,345, silver jumped 4–5%, platinum gained more than 4%, and palladium more than 5%.

The second force landed Wednesday and undid much of the first. Kevin Warsh chaired his first FOMC meeting, and while the committee held the benchmark rate at 3.50–3.75% as expected, the message around it was pointedly hawkish. The statement was stripped of forward guidance entirely. Warsh declined to submit his own projection to the “dot plot,” becoming the first Fed chair in 14 years to sit out the forecast. The projections that were submitted now point to about 25 basis points of hikes in 2026, with nine of eighteen officials expecting a hike this year, and the committee lifted its 2026 inflation outlook toward 3.6%. The dollar surged to its highest level since May 2025.

Metals gave the Monday gains back. Gold slid below $4,200 on Thursday as the hawkish reading and the stronger dollar sank in, and silver posted its sharpest single-day drop in weeks before recovering nearly 70% of the move. Friday’s Juneteenth session is thin, with gold ticking back toward $4,350 and silver near $71, but the medium-term trend is still lower; gold is heading toward roughly its third straight weekly loss despite the midweek pop. For all the drama of the Iran deal, a Fed that has stopped talking about cuts set the week’s direction.

Track live precious metals prices →

A Record Share of Central Banks Plan to Buy More Gold

The most durable story of the week came from the official sector. The World Gold Council’s 2026 Central Bank Gold Reserves Survey, released this week, found a record 45% of central banks expect to increase their own gold reserves over the next 12 months — and 89% expect global official reserves to keep rising. Central banks have averaged roughly 1,000 tonnes of gold purchases a year over the past four years, double the prior decade’s pace, and by some measures gold has now overtaken U.S. Treasuries as the world’s largest reserve asset. Just as telling, 74% of respondents expect the U.S. dollar’s share of global reserves to shrink within five years, while 84% see gold taking a larger share, up from 76% a year ago.

This is the structural counterweight to the hawkish Fed. The official-sector bid is not reacting to one meeting or one inflation print; it reflects a multi-year reserve-diversification decision made by institutions that do not trade on next week’s dollar move. It is the floor under the price even in a week when the price fell.

The Silver Squeeze You Can’t See on the COMEX Screen

Underneath silver’s volatility sits a quieter physical story. Silver on the Shanghai Gold Exchange has been trading around 8% above the Western spot price — roughly $73 an ounce against about $67 on COMEX in mid-June — and that premium has held in the high single digits to mid-teens for weeks. At the same time, COMEX warehouses hold about 319 million ounces of silver, but only an estimated 82–85 million of those are “registered” and actually available for delivery.

The force pulling physical silver east is industrial. China manufactures more than 80% of the world’s solar panels, and solar alone now consumes roughly a fifth of annual global silver supply. Silver is also in the electronics supply chain that runs through every phone and laptop — the same week these inventory figures printed, Apple was reported to be weighing iPhone price increases of 4–6% on tariffs and rising component costs. Silver is not the reason a phone gets more expensive; tariffs and memory chips are. But it is a useful way to see the bigger picture: the metal that is quietly commanding an 8% premium in Shanghai is the same metal embedded in the devices and panels whose costs keep climbing. The paper price you see quoted on COMEX is only part of the story.

A 22.5-Pound Atocha Silver Bar Surfaces — the First Since 1999

Collectors got a striking piece of history this week. Mel Fisher’s crew recovered a 22.5-pound silver bar from the wreck of the Nuestra Señora de Atocha, the Spanish galleon that sank in a 1622 hurricane off the Florida Keys. It is the first silver bar the team has pulled from the site since June 1999, brought up from about 50 feet of water roughly 404 years after the ship went down. The company estimates it at around $100,000, though some reports put it as high as $200,000. Silver bars were among the Atocha’s primary cargo, and hundreds more, along with thousands of coins and Colombian emeralds, remain undocumented on the seabed — a reminder of how long silver has served as a store of value.

Premium vs. Melt: The UFC “Freedom 250” Coins

A different kind of silver-and-gold story made the rounds this week: a set of commemorative “Freedom 250” medallions tied to the first UFC championship held at the White House. The pieces range from a one-ounce silver medallion at $249.99 to a one-ounce gold medallion at $11,999.99, with a five-ounce silver and a tenth-ounce gold in between. Set the politics aside and there is a useful bullion lesson here. A one-ounce gold medallion priced near $12,000 against a spot price around $4,300 carries roughly a $7,700 premium for branding, packaging, and grading. That is the difference between buying metal and buying a collectible — a distinction every new buyer should understand before they pay up.

What We’re Watching

The Fed regime change is the dominant story now. With forward guidance gone and the chair declining to forecast, markets have less to lean on, and every data point between now and the next meeting will swing the dollar and the metals with it. The Iran agreement is the wildcard in the other direction — it is an interim MOU, not a signed treaty, and any breakdown would push oil and the inflation trade right back up. Beneath both sits the central-bank bid — the strongest hand in this market, and the one not trading the headlines at all.

")