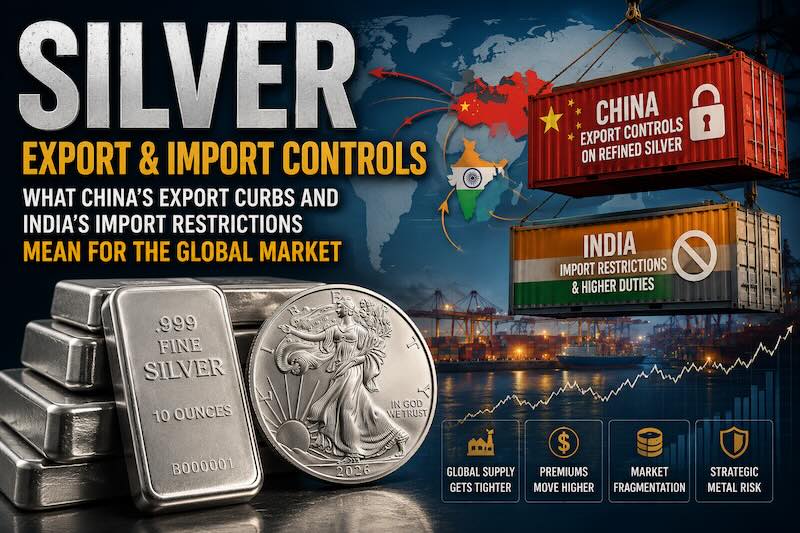

China imposed export controls on refined silver in January 2026. India hiked import duties from 6% to 15% and restricted most silver imports in May. Two countries that collectively consume and refine more silver than anyone else — both restricting the flow of physical metal across their borders within six months of each other.

The global silver market was already running a structural supply deficit. These moves make it tighter.

What China Did

China mines about 13% of global silver output but refines 60–70% of globally traded silver. That refining bottleneck is the leverage point. Starting January 1, 2026, Beijing replaced its quota system with a licensing framework limiting silver exports to 44 state-approved companies. Exporters must produce at least 80 tonnes annually and carry $30 million in credit lines — requirements that shut out small and mid-sized refiners.

About 120 million ounces of annual silver exports now flow through a government-controlled gate that Beijing can widen or narrow based on domestic industrial needs. Those needs are growing: China’s solar panel manufacturing consumes enormous volumes of silver, and the country posted record silver imports in March 2026 while simultaneously restricting exports. Import more raw material, retain domestic refining output, build a strategic industrial reserve. Same playbook China ran with rare earth elements — control the refining bottleneck and you don’t need to control the mines.

The Shanghai silver price has traded at a persistent premium to London and COMEX since these controls took effect. That spread is a real-time measure of how the restrictions are splitting global pricing.

What India Did

India is the world’s largest silver consumer, importing over 90% of its silver. Silver imports hit $12 billion last fiscal year, up from $4.8 billion the year before. That surge, combined with a rupee hitting record lows near 97 per dollar, forced the government’s hand.

May 13: import duties on gold and silver hiked from 6% to 15%. May 16: most silver imports restricted with immediate effect.

Domestic silver prices jumped 5–6%, less than the full 9% duty increase because dealers were still working through inventory bought at old rates. As those stocks deplete, the full cost hits. The India Bullion and Jewellers Association told members to stop selling bullion directly to customers and limit sales to five grams. Silver ETFs in India started trading at widening premiums over net asset value.

Industry sources inside India warned that silver faces steeper challenges than gold from these restrictions because silver’s supply channels are more concentrated. The IBJA also proposed monetizing nearly 1,000 tonnes of idle “temple gold” held by religious trusts to reduce gold import dependence — India spends roughly 800 tonnes of gold imports per year, its second-largest foreign exchange outflow.

What It Does to Global Supply

Annual silver mine production runs about 830 million ounces. Total supply including recycling hits roughly 1 billion. Demand exceeded 1.2 billion ounces in 2025 — a deficit north of 200 million ounces, roughly equal to Mexico’s entire annual output. That deficit has persisted for five consecutive years.

China restricting exports and India restricting imports don’t cancel each other out. They fracture the market into regional pools with different pricing and availability. Silver that would have moved from Chinese refiners to Indian buyers now stays in China, gets redirected to Western markets, or enters smuggling channels at higher premiums.

Silver lease rates — what institutions pay to borrow physical metal — hit 8% annualized in early 2026. When someone pays 8% just to borrow silver for delivery, the physical market is signaling a supply-demand imbalance that the spot price alone doesn’t capture.

Track the COMEX silver price alongside the Shanghai premium to watch the divergence.

Could More Countries Restrict Silver?

Silver is critical for solar panels, EV electrical systems, 5G infrastructure, and defense. The IEA estimates solar and EV sectors alone will consume half of global silver output by 2030. That makes silver a strategic industrial metal, not just a monetary one — and strategic metals attract export controls.

Countries with significant silver production like Mexico, Peru, Chile, Russia, and Poland are watching. Russia’s domestic precious metals demand surged 350% year-over-year in early 2026. The rare earths precedent is clear: China restricted exports, prices spiked, markets permanently restructured around higher costs and fragmented supply. Silver appears to be following the same arc.

What U.S. Buyers Should Watch

Most physical silver sold by American dealers comes from domestic mining, North American refining, and existing inventory — not directly from Chinese exports. But silver is priced globally. When 120 million ounces get pulled behind an export gate and India’s import channels constrict, the ripple effects reach COMEX pricing and dealer premiums.

During previous supply disruptions, U.S. dealer premiums on bars and rounds expanded from their normal 3–6% range to 15–30% or higher. Whether these restrictions trigger that kind of expansion depends on enforcement and duration.

The closest-to-spot silver page ranks every silver product by premium over spot across major dealers. During tight-supply periods, the spread between the cheapest and most expensive dealer on the same product widens. It’s always a good idea to comparison shop prices and premiums when you are looking to buy silver. The Shanghai silver price relative to COMEX is the leading indicator: when Shanghai trades at a persistent premium, that pricing pressure is likely to eventually transmits west.

")